Starting from January 1, 2024, the on-grid electricity price for coal power will formally consist of two components: “capacity tariff + energy price”, departing from the previous single-price system. The capacity tariff charges for coal-fired power will be included in the power system’s operational costs, which will be shared among industrial and commercial users based on their monthly power consumption. This initiative aims to establish a sustainable mechanism for supportive power sources and ensure supply security.

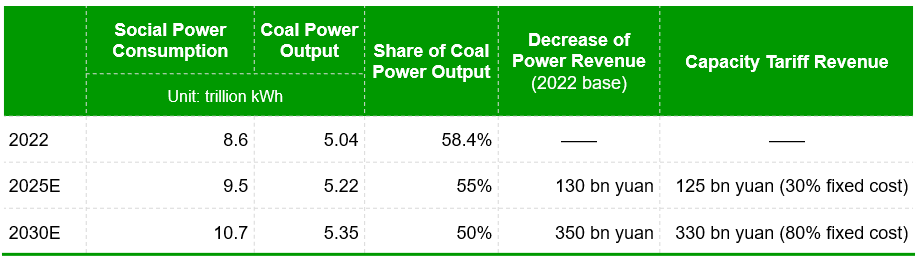

The capacity pricing mechanism and ancillary services are set to be the main pathways for the sustainable operation of newly installed units. With the substantial increase in renewable power installation and power demand, the utilization hours of coal-fired power have been declining. It is difficult for enterprises to fully recover costs under the single-price system. After the reform, there are 33 provincial-level power grid regions with coal-fired power capacity tariffs ranging from 100-165 yuan/kW-year for 2024-2025. According to preliminary estimates by GL Consulting, when China’s coal power output share drops to 50%, the revenue from capacity tariff charges could basically cover the decline in power volume income.

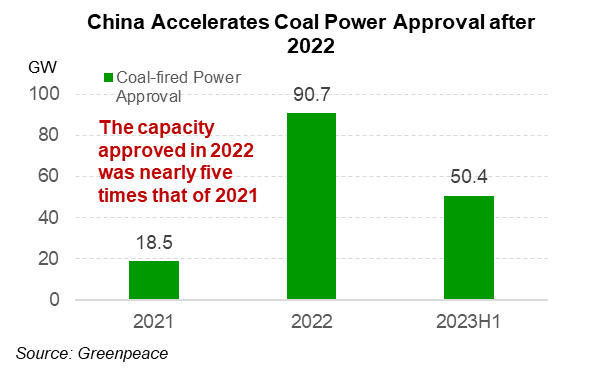

China’s electricity demand continues to grow with tighter peak hour supply. In recent years, China has accelerated coal power approval, with new units expected to be completed successively around 2025, when the total installed coal power capacity in China is projected to be around 1300GW, nearing to the 2023 peak power load of 1370GW in 2023. With the expanding electrification of end-users, the power load is likely to continue increasing. The Global Energy Interconnection Development and Cooperation Organization (GEIDCO) estimated that China’s peak power load will reach 1570GW by 2025 and 1820GW by 2030, indicating a gap in stable power capacity during peak periods.

Forecast of Capacity Tariff Revenue with Lowering Coal Power Shares

Source: GL Consulting

China’s electricity demand continues to grow with tighter peak hour supply. In recent years, China has accelerated coal power approval, with new units expected to be completed successively around 2025, when the total installed coal power capacity in China is projected to be around 1300GW, nearing to the 2023 peak power load of 1370GW in 2023. With the expanding electrification of end-users, the power load is likely to continue increasing. The Global Energy Interconnection Development and Cooperation Organization (GEIDCO) estimated that China’s peak power load will reach 1570GW by 2025 and 1820GW by 2030, indicating a gap in stable power capacity during peak periods.

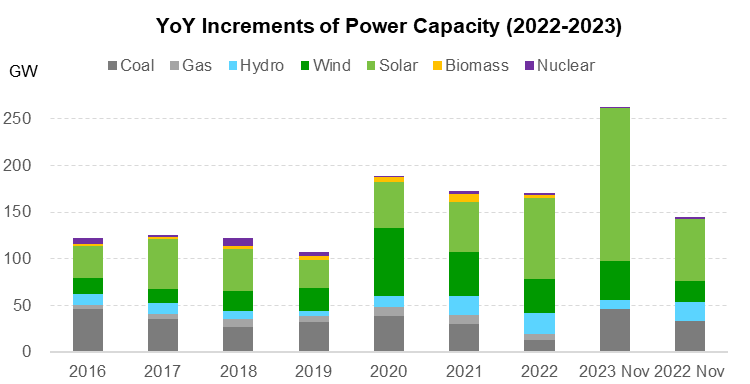

Source: CEC, NEA, GL Consulting