The global gas market remains under pressure even after the apparent easing of U.S.-Iran tensions. Oil flows through the Strait of Hormuz have started to recover, but LNG shipments from Qatar remain heavily disrupted after renewed Iranian attacks on vessels. That matters because Qatar is one of the world’s largest LNG exporters and accounted for roughly one-fifth of global LNG supply before the conflict.

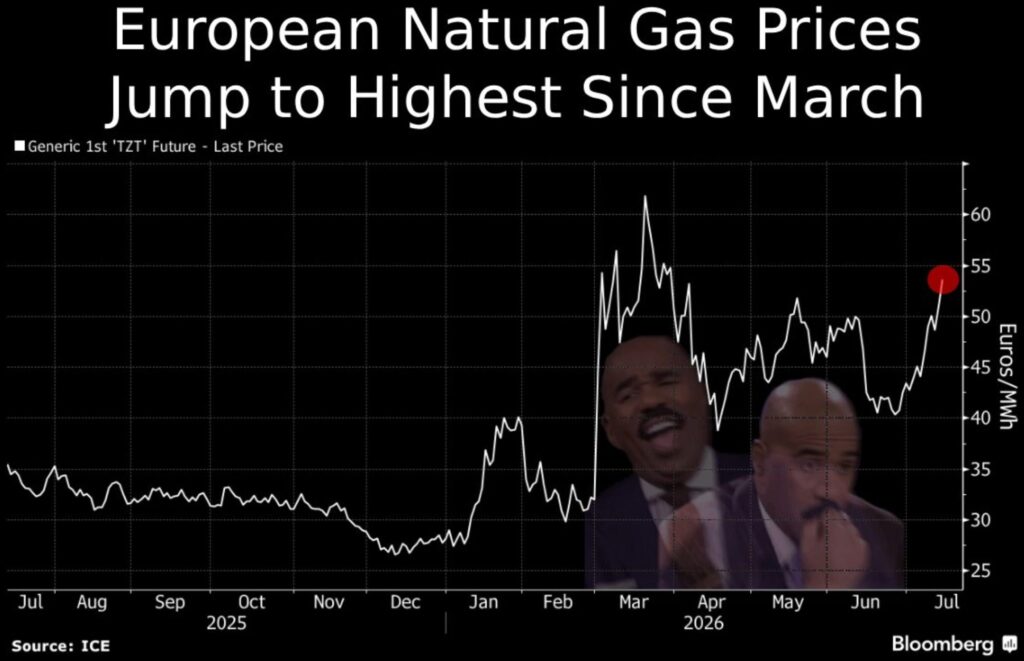

News headlines are focusing on how crude prices have retreated toward prewar levels, but benchmark LNG prices remain about 70% above where they were at the end of February. The market is clearly treating LNG supply risk as more persistent and more serious than oil supply risk.

The immediate concern is Qatar’s Ras Laffan complex, the world’s largest LNG export facility. Before the latest vessel attacks, empty LNG tankers were lining up near Qatar in anticipation of a restart. Instead, shipments remain near-paralyzed. One of the recently struck vessels was carrying Qatari crude, likely raising concerns around crew safety, insurance costs, and the willingness of shipowners to move cargoes through the Gulf.

Restarting Ras Laffan may also be more complicated than the market initially assumed. LNG facilities are technically complex, and a recent explosion and fire at a separate domestic gas plant, which killed 13 people and injured 66, has added to concerns about operational delays. QatarEnergy has said the accident should not affect LNG shipments, but its commercial behavior suggests otherwise: the company has extended force majeure on some shipments to Asia and Europe and continues to sublease vessels, both signs that exports may not rebound quickly.

For Europe, the timing is particularly bad. The region entered the restocking season with storage only 28% full after a cold winter, and inventories are currently around 48% full, below normal. Wood Mackenzie expects EU storage to end the injection season at just 76%, the lowest level since at least 2011. Goldman Sachs estimates that if Ras Laffan is back at full capacity by the end of July, Europe may end the season around 74% full; if the restart is delayed by another month (a distinct possibility), storage could be closer to 70%. Both scenarios are below the European Commission’s advised minimum of 75%.

That creates meaningful winter price risk. Energy Aspects reports that speculative positioning is increasingly betting on higher winter European gas and LNG prices. Wood Mackenzie has noted that prices could soften in the near term if geopolitical news improves, but winter risks remain skewed to the upside.

Asia remains exposed. Major LNG buyers may be forced deeper into the expensive spot market or look to coal for power generation. For countries such as Pakistan and Thailand, LNG is central to economic growth and plans to reduce coal use — but only if LNG is affordable. If prices stay elevated, buyers will conserve gas demand, delay purchases, or turn back to coal and other fuels where available.

The key takeaway is that the expected LNG market loosening may be delayed. Supply growth is still coming over the next few years, but low European storage leaves the market with little margin for error heading into winter.

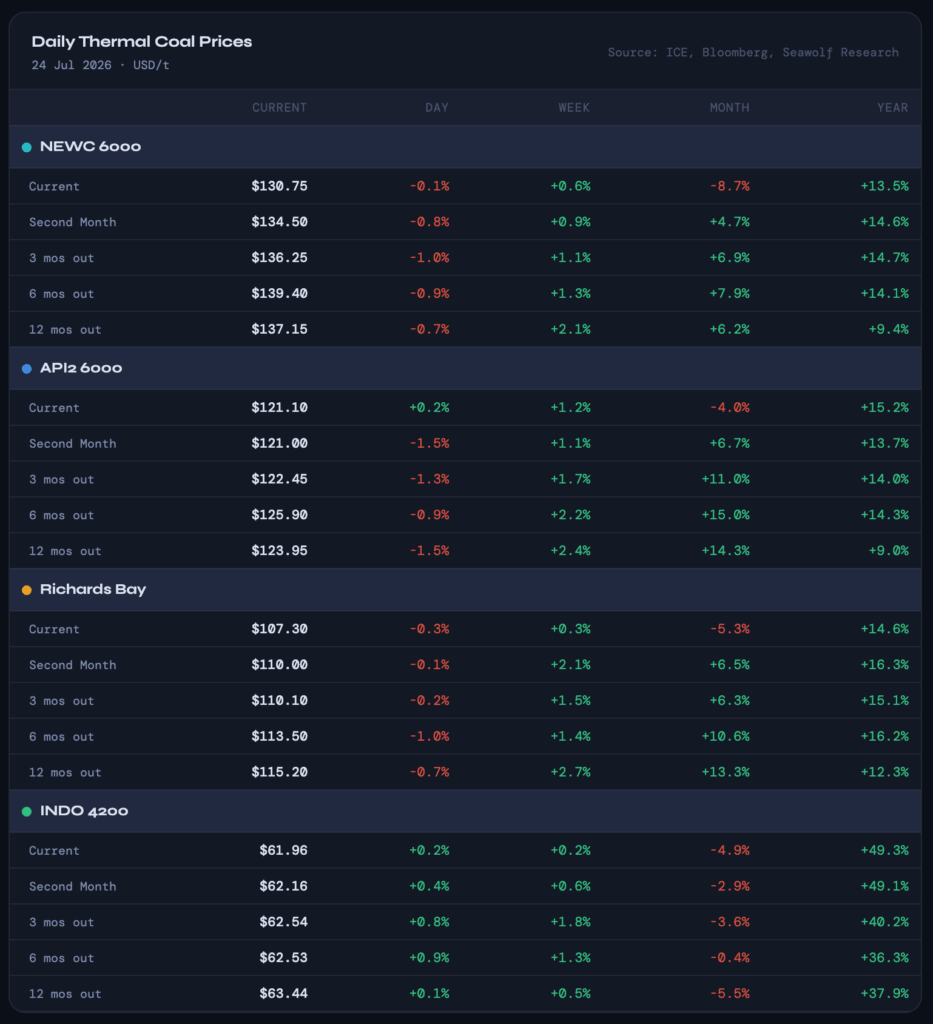

For thermal coal investors, this is supportive at the margins. Expensive LNG and European gas will improve coal’s competitiveness with gas in Europe and Asia, especially where coal plants remain available and gas affordability becomes a political or economic constraint. The clearest beneficiaries are likely seaborne thermal coal producers with exposure to Asian demand.

-JA