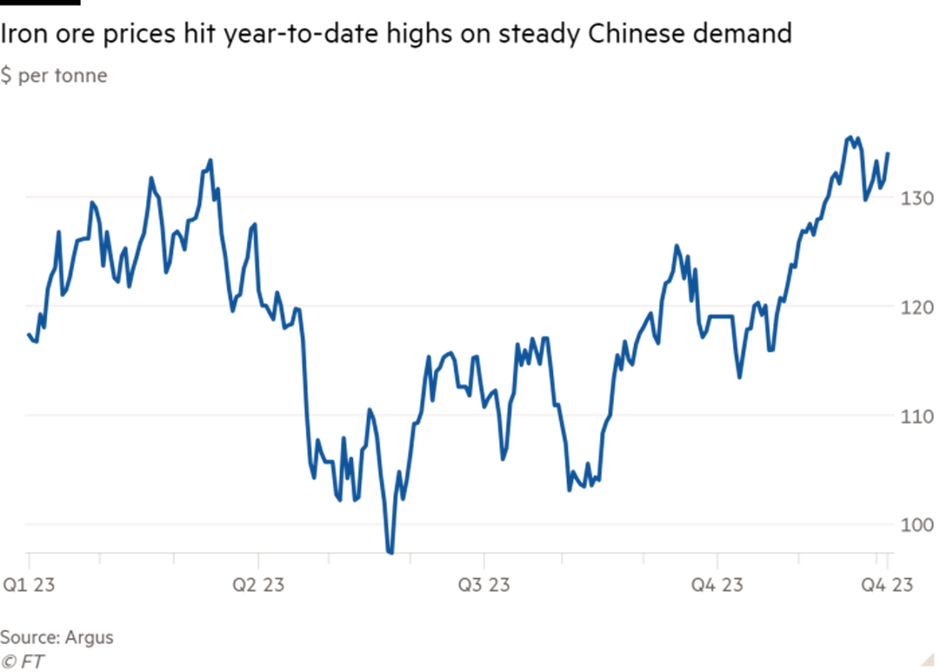

Iron ore prices have defied investors’ expectations and climbed by almost two-fifths since May, driven by a surge in Chinese steel production in spite of the near collapse of the country’s real estate sector. Prices for the bulk commodity, a crucial ingredient in steel, have climbed 38 per cent over the past seven months to $133.95 a tonne, Argus data shows.

The rally has taken off since August. Analysts say the spark was Chinese officials telling steel manufacturers that an annual production cap would not apply this year, in a bid to prop up the country’s flagging economic growth. The steel industry has since gone into overdrive, with output for the second half of this year on track to be the second strongest on record behind 2020, according to Goldman Sachs.

As a result, steel prices have fallen as China has flooded the market. But prices of iron ore, of which China is by far the biggest buyer, have jumped at the same time.

China’s robust demand for iron ore — it has imported 1.1bn tonnes this year, mostly from Australia and Brazil, up 6 per cent on the first 11 months of 2022 — has come despite a sharp drop in demand for property construction, as developers have buckled under the weight of large debt piles. A pipeline of government-backed infrastructure and manufacturing projects has only partially offset the real estate downturn.

However, steelmakers have been able to sell their excess supply abroad, and have been helped by the yuan’s year-to-date slide against the dollar. Many producers have therefore increased their output, supporting demand for iron ore, even though their margins have been squeezed. Speculators betting that China’s property crisis would mean lower prices for iron ore have been burnt.

“If you go back to the second quarter, one of the highest conviction trades at big US banks was to short iron ore, but it goes into so much more than just houses,” said Tor Svelland, chief executive at commodity-focused hedge fund Svelland Capital.

“We never thought the government would allow a surge in exports of steel, but they did,” said Tom Price, an analyst at Liberum. “Economic growth is so weak [that] they allowed the steel industry to continue unconstrained.” Analysts at Morgan Stanley in May had said they expected prices would be about $90 a tonne by the fourth quarter. Ewa Manthey, commodities strategist at ING, now expects prices to average around $120 a tonne in 2024 if Beijing introduces further stimulus measures to support the economy.

Meanwhile, spot prices for dry bulk ships have surged as Brazilian iron ore miners benefiting from dry weather linked to the El Niño effect compete with thermal coal traders for space aboard a limited number of vessels. The Baltic Dry index, which tracks rates for huge, non-container-carrying ships, soared to its highest level since May 2022 in the first week of December, though it has since dropped 25 per cent.

Capesize bulkers, which have a capacity of up to 200,000 deadweight tonnes and typically carry iron ore and coal, were able to charge just over $54,000 a day on December 4, when the BDI peaked, up from just over $17,000 a day one month earlier, according to Clarksons Securities.