China faced difficulties to increase its coking coal supply notably in 2023, as the country’s frequent safety inspections following soaring coal mine accidents in the latter half of the year had temporarily put operations of some mines on hold, according to Mysteel’s annual report on the commodity released on January 8.

For example, in Shanxi alone, China’s largest coking coal mining province, the number of coal mine accidents had soared to 87 as of November 18 through 2023, up by a significant 61% on year, according to a document issued by the country’s State Council.

Mysteel’s survey has also showed several marked output drops of the coke-making material in end-June, late-September and mid-November last year, respectively, due to stricter safety checks incurred by coal mine accident concealment as well as severe accidents.

Moreover, there was limited additional coking coal production capacity actually put into construction in 2023, due to China’s strict scrutiny over new coal capacity as well as relatively long construction period before their commissioning, according to the report.

As a result, China’s coking coal supply last year only edged up by a meagre 0.3% compared with the previous year, according to Mysteel’s estimation. The figure was in stark contrast with a 2.9% growth that had already been logged in the country’s total raw coal production in the first 11 months last year, according to data from the National Bureau of Statistics.

However, coking coal availability for Chinese users stayed relatively loose last year, mainly due to sufficient supplement of imported coking coal cargoes that were quickly boosted by China’s record high hot metal production as well as its extended policy of zero import coal tariffs to the end of 2023, said the report.

Specifically, China received about 90.63 million tonnes of coking coal shipments from other countries in the first 11 months last year, up by a marked 58% on year, according to the data from country’s General Administration of Customs.

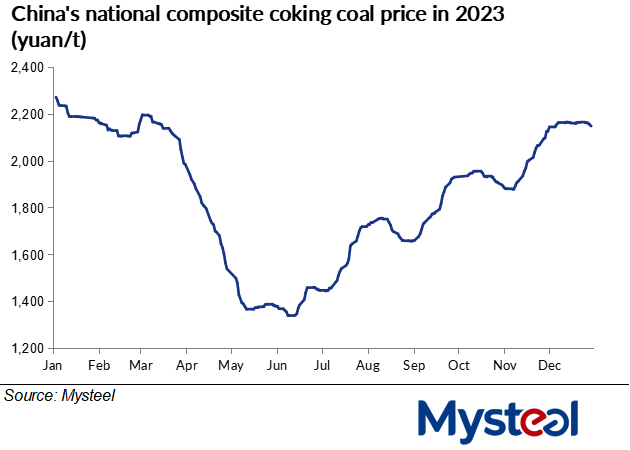

This situation has led domestic coking coal prices to fluctuate more with changes in downstream demand. For example, the domestic steel market remained in the downturn in the first half (H1) of last year as a result of a slumping property market, the report argued, with China’s national composite steel price assessed by Mysteel touching an intra-year low at Yuan 3,903.27/t on May 31.

The sluggish steel market in H1 obviously capped mills’ production at blast furnaces, with hot metal output at 247 Chinese steel mills under Mysteel’s survey averaging 71.63 million tonnes in H1.

But in the second half year (H2), their average output increased by 2.9% from H1 to 73.68 million tonnes as encouraged by a raft of favourable macro policies, and the volume was also higher by 5.3% than the comparable months in 2022, the survey results showed.

Accordingly, China’s coking coal prices showed a V-shaped trend in 2023, with prices climbing up in H2 from lows in June. But still, the average level of China’s national composite coking coal price under Mysteel’s assessment last year was still lower by Yuan 476.3/tonne ($66.4/t) on year to sit at Yuan 1,843.2/t, as downstream users frequently slipped into losses or suffered meagre profits.

In addition, impacted by the domestic coking coal market, import prices of coking coal from Mongolia, China’s largest supplier of the feedstock, also displayed a similar V-shaped trend in 2023, bottoming out at Yuan 1,045/t on June 14, Mysteel Global learned.

In 2024, China’s coking coal market is expected to see a mild glut that will pose downside risks to the prices, the report predicted, citing that elevated imports will push up the supply while the demand is likely to slip due to lower hot metal output at mills.