Whitehaven Coal ($WHC.AX, $WHITF) delivered a solid performance in the December 2024 quarter, with clean coal production increasing and sales volumes rising across both its operating divisions in Queensland and New South Wales. The company remains on track to hit the upper end of its full-year production guidance while keeping unit costs at the lower end of expectations.

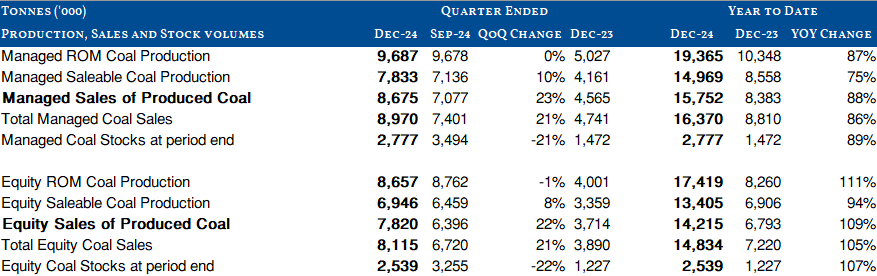

Whitehaven produced 7.8 million tonnes of clean coal in the quarter, a 10% increase from the September quarter. Sales of produced coal rose 23% to 8.7 million tonnes amidst strong demand, with metallurgical coal accounting for 63% of total sales revenue. The company also reduced its net debt to A$1.0 billion, down from A$1.2 billion at the end of September.

In Queensland, Whitehaven’s Daunia and Blackwater mines produced 3.6 million tonnes of clean coal, a 7% decline from the prior quarter due to seasonal weather disruptions. Despite this, Queensland coal sales increased by 28% to 4.6 million tonnes, supported by strong customer demand and improved rail logistics. Whitehaven achieved an average coal price of A$237 per tonne, equivalent to 75% of the Platts PLV HCC Index. The company continues to focus on cost reduction initiatives, aiming to achieve A$100 million in annualized savings by the end of FY25.

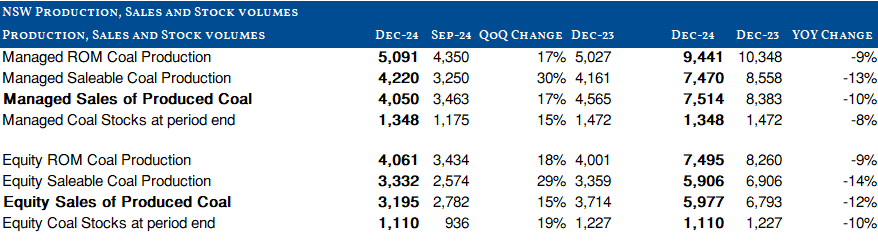

New South Wales operations also posted a strong quarter, with clean coal production rising 30% to 4.2 million tonnes, supported by improved performance at the open-cut mines. Sales of NSW-produced coal increased 15% to 3.2 million tonnes, with an average realized price of A$211 per tonne, in line with global benchmarks. Narrabri’s underground production was steady for most of the quarter, though an unplanned December outage impacted volumes. A planned eight-week longwall move is scheduled to begin in late February, which will reduce output in the second half of the fiscal year.

Looking ahead, Whitehaven remains optimistic about coal market fundamentals despite short-term price volatility. The company expects metallurgical coal prices to remain solid as global supply constraints persist and demand from India grows. Thermal coal demand, particularly from Japan, remains firm, with winter conditions expected to support pricing.

Whitehaven’s financial flexibility is expected to improve further in the coming quarter, with the expected receipt of US$1.08 billion from the sale of a 30% stake in Blackwater. The company continues to advance its Narrabri Stage 3 Extension, which extends mine life to 2044, and is progressing the Winchester South metallurgical coal project, now under regulatory review, with a Queensland Land Court hearing scheduled for July 2025.

Source: Company Filings